Economics

Monthly UK Economic Outlook: November

Our economists share their views on the key economic trends to watch in the month ahead.

21 Nov 2023

. 4 min read

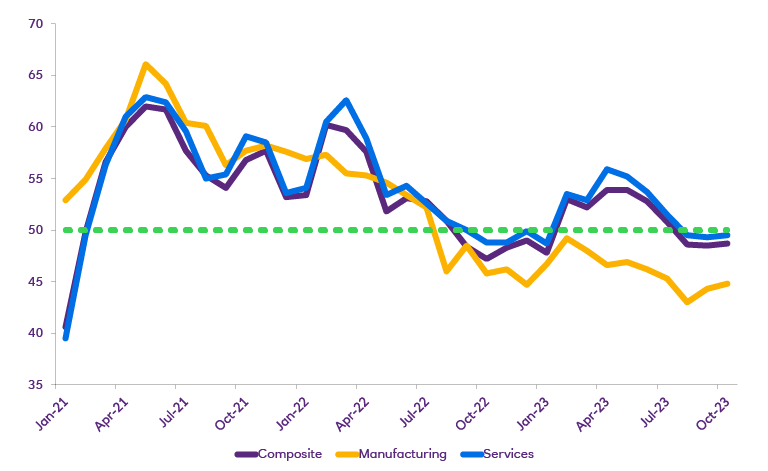

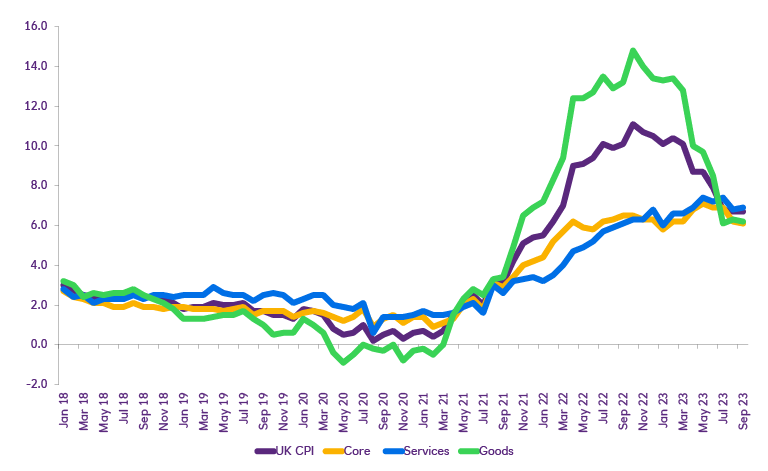

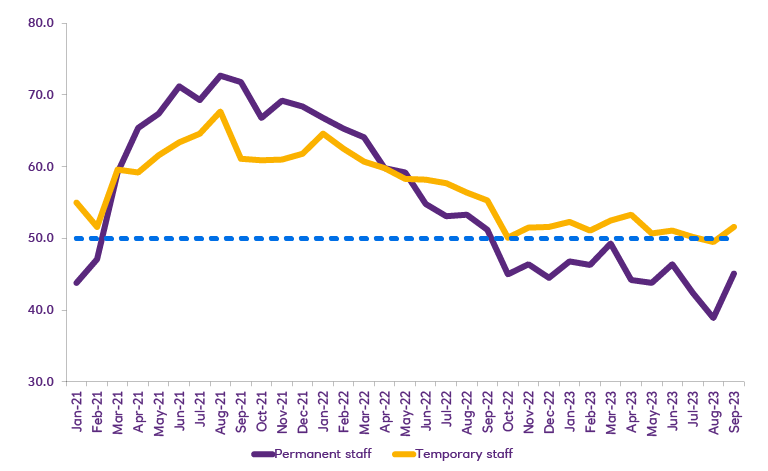

It’s often said that monetary policy operates with long and variable lags. The rate tightening cycle that got underway two years ago now seems to be biting a little harder, with the UK economy not growing in Q3. To be fair, while that reflects the impact of rising borrowing costs, both public sector strikes and weather-related disruptions also played a part.